Which States Have No Corporate Income Tax in 2026?

Picking a state based on its corporate income tax rate alone is a shortcut that tends to backfire. The usa corporate tax rate by state picture is messier than a single number. Some states advertising zero corporate income tax, like Texas and Ohio, replace it with gross receipts taxes that don't care whether your business is profitable. Others, like South Dakota and Wyoming, genuinely offer a low-tax environment across the board. And then there's the federal corporate tax rate sitting at 21% regardless of where you're registered. If you want to know which states on the list of states with no corporate income tax actually deliver on that promise in 2026, this is the breakdown worth reading.

TLDR:

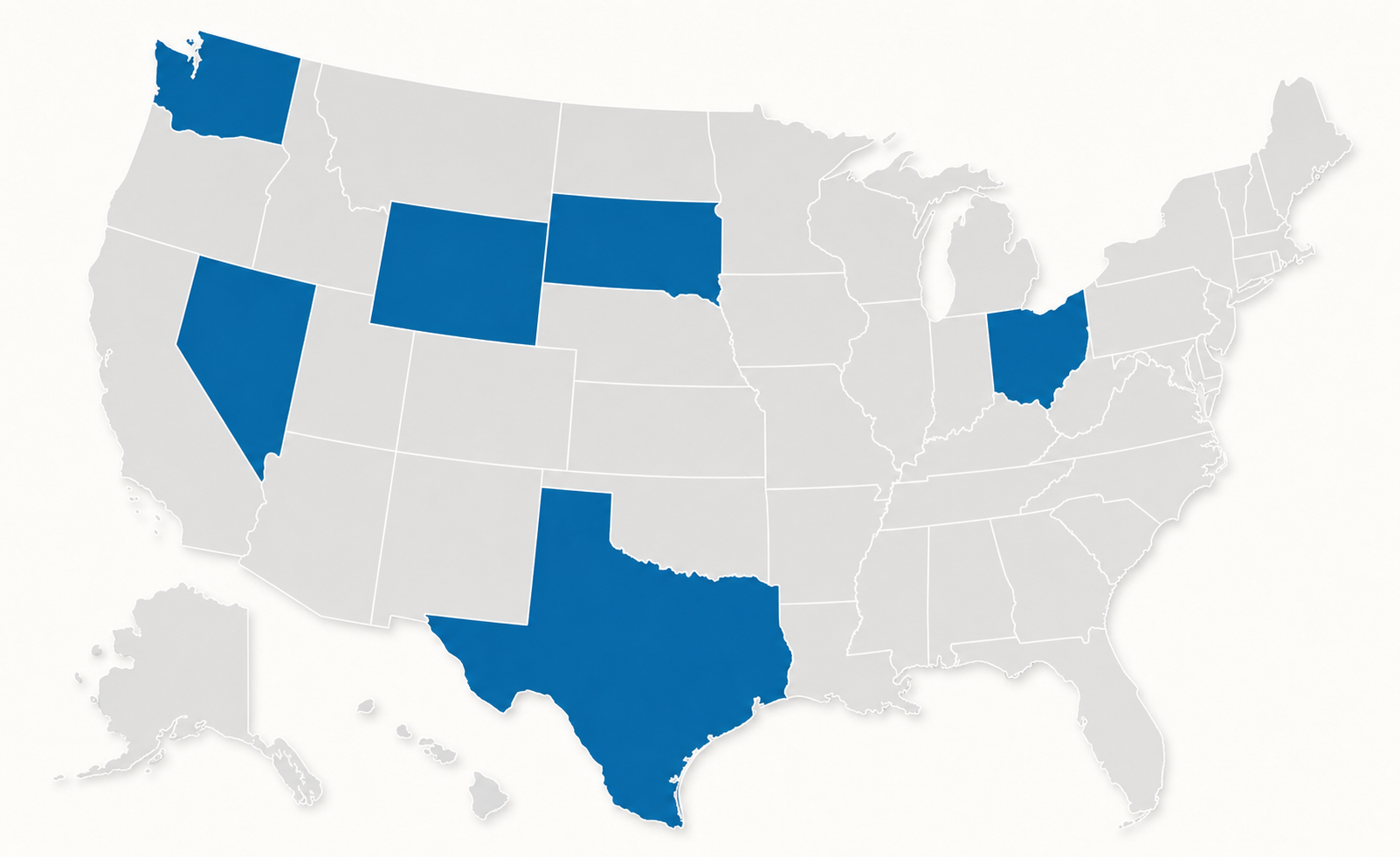

- Six states have no corporate income tax in 2026: Nevada, Ohio, South Dakota, Texas, Washington, and Wyoming.

- Most of those states replace corporate income tax with gross receipts or franchise taxes, so your real burden depends on revenue over profit alone.

- Your 21% federal corporate tax rate applies regardless of where you register or operate.

- Remote team members can create tax nexus in states you never registered in, triggering withholding and filing obligations.

- Bolto handles multi-state payroll and compliance for distributed teams across multiple jurisdictions.

The Federal Corporate Tax Rate: The Foundation Every Business Starts With

Before your state tax picture comes into focus, you need to understand what every U.S. business pays at the federal level first.

The federal corporate income tax rate is a flat 21%, set by the Tax Cuts and Jobs Act of 2017. That rate applies to C corporations on their taxable net income. It does not apply to pass-through entities like S corporations, partnerships, or sole proprietorships, which pass income through to owners who then pay individual income tax rates instead.

Here is what that looks like in practice:

- C corporations pay 21% on taxable net income at the federal level, before any state taxes are layered on top.

- S corporations generally pay no federal corporate income tax at the entity level. Income flows to shareholders, who report it on personal returns.

- LLCs are taxed based on their elected classification, either as a disregarded entity, partnership, or corporation, so the federal rate may or may not apply depending on how the entity is structured.

State corporate taxes are separate from and in addition to the federal rate. So when a state advertises zero corporate income tax, that means no state-level tax on corporate income, not a reduced federal obligation. Your 21% federal liability stays regardless of where you register or operate.

This distinction matters because some of the most popular low-tax states, like Texas and Nevada, still carry real tax costs through franchise taxes, gross receipts taxes, or other levies that can offset the headline benefit of "no corporate income tax."

This content is for general informational purposes only and does not constitute legal or tax advice. Tax rules vary by situation and change over time. Consult a qualified tax professional for guidance specific to your business.

How State Corporate Income Taxes Work

Most businesses focus on federal taxes, but state corporate income taxes can meaningfully shift your total tax burden. Here's how the system actually works.

The federal corporate tax rate sits at 21% for most corporations, but states layer their own taxes on top of that. Some states tax corporate net income directly, others use a gross receipts or franchise tax structure, and a handful impose no corporate income tax at all.

What Gets Taxed Varies by State

States generally use one of three approaches:

- A net income tax, which mirrors federal taxable income with state-level adjustments. Most states follow the federal definition of income, then apply their own additions and subtractions before calculating what you owe.

- A gross receipts tax, which taxes total revenue before any deductions. Texas uses this structure through its franchise tax, which applies to gross revenues over $2.47 million at a 0.75% rate for most businesses.

- A franchise or privilege tax, which charges businesses for the right to operate in the state, not on income earned. Delaware is well known for this model.

How States Apportion Income

If your business operates in multiple states, each state typically claims a share of your taxable income based on an apportionment formula. Most states now use a single-sales factor, weighting where your customers are located over where your employees or property sit. This matters because a company with substantial sales into a high-tax state may owe taxes there even without a physical office.

State corporate tax rates range from roughly 2% to over 11%, so where you do business, and where you're registered, can have a real impact on what you pay.

The Six States With No Corporate Income Tax in 2026

As of 2026, six states levy no corporate income tax, though most replace that revenue through alternative tax structures that can still create real obligations for businesses operating within their borders.

Here is a look at each state and what it collects instead.

The Six States and Their Alternative Tax Structures

| State | How the State Generates Business Revenue |

|---|---|

| Nevada | Commerce Tax on gross receipts above $4 million; statewide sales tax |

| Ohio | Commercial Activity Tax (CAT) applied to gross receipts |

| South Dakota | Sales and use tax; no individual income tax either |

| Texas | Franchise tax (the "margin tax") based on revenue or profit margin |

| Washington | Business and Occupation (B&O) tax on gross receipts |

| Wyoming | Severance taxes on natural resources; sales tax |

The absence of a corporate income tax does not always mean a lighter overall tax burden. Texas, for example, applies its franchise tax to most businesses with revenue above $2.47 million, calculated as a percentage of taxable margin. Washington's B&O tax applies to gross receipts regardless of profitability, which can be meaningful for businesses with thin margins. Nevada and Ohio both tax revenue instead of profit through their respective gross receipts structures.

South Dakota and Wyoming come closest to offering a genuinely low business tax environment, with neither state imposing a corporate income tax nor an individual income tax. That combination makes them popular choices for holding companies and pass-through entities in particular.

Gross Receipts Taxes: What "No Corporate Income Tax" Really Means

Gross receipts taxes work differently from corporate income taxes, and the distinction matters more than most business owners realize. A few of the states that advertise zero corporate income tax still impose a gross receipts tax, which is calculated on total revenue before any expenses are deducted. That means you pay regardless of whether your business is profitable.

States That Have Gross Receipts Taxes Instead

Texas and Washington are the two most common examples here. Texas levies its franchise tax on gross revenues above a certain threshold, and Washington's Business and Occupation (B&O) tax applies to gross income from business activities. Neither state calls it a corporate income tax, but the financial obligation is real.

- Texas imposes its franchise tax at a rate of 0.375% for retailers and 0.75% for most other businesses, with revenues under $2.47 million generally exempt.

- Washington's B&O tax rate varies by industry, ranging from 0.138% for manufacturing to 1.5% for service businesses, with no deduction for cost of goods or payroll.

- Ohio replaced its corporate income tax with a commercial activity tax (CAT) on gross receipts, so profitable and unprofitable businesses are taxed at similar rates.

The practical implication: a high-revenue, low-margin business could pay more in gross receipts taxes than it would under a traditional corporate income tax structure. Before choosing a state based on its "no corporate income tax" status, confirm whether a gross receipts or commercial activity tax applies to your industry and revenue level. Consulting a qualified tax professional for your specific situation is the right call before making any structural decision.

Notable Low-Rate States Worth Comparing

Even without eliminating corporate income tax entirely, several states keep rates low enough to matter when you're deciding where to register or expand.

States That Come Close

Pennsylvania cut its corporate net income tax from 9.99% to 8.99% in 2023, with a phased reduction plan targeting 4.99% by 2031. New Jersey sits at 9% for most corporations, though it layers in a minimum tax and surcharges that can push the effective burden higher. New York's general corporate franchise tax rate is 7.25%, but New York City adds its own tax on top, making the combined rate one of the steeper ones in the country.

Why Rate Alone Can Mislead You

A headline rate rarely tells the full story. Consider what else each state layers on:

- Gross receipts taxes or franchise taxes that apply regardless of profitability, like Texas's franchise tax, which is structured around revenue instead of net income

- Local income or business taxes, especially relevant in cities like New York City, which imposes its own corporate tax separate from the state

- Sales tax rates and county-level variations that affect day-to-day costs if you're selling goods or services locally

- Capital base taxes, which some states charge even when a business runs at a loss

Comparing states purely on their corporate income tax rate misses these compounding costs. Your actual tax burden depends on entity type, revenue structure, where your customers are located, and how each state defines taxable income.

States With the Highest Corporate Tax Rates

Here is a look at the states where corporations face the steepest tax burdens, which matters for context when weighing relocation or expansion decisions.

Several states stand out for their high corporate income tax rates in 2026:

- New Jersey applies the highest corporate income tax rate in the country at 11.5%, which applies to corporations with income over $1 million. Smaller businesses face a 6.5% rate, though the top bracket makes New Jersey a costly home for profitable companies.

- Minnesota charges a top corporate income tax rate of 9.8%, making it one of the steeper state-level burdens in the Midwest for mid-to-large businesses.

- Illinois imposes a flat 9.5% corporate income tax rate, which includes the base 7% rate plus a 2.5% personal property replacement tax. Every corporation pays this regardless of size or income level.

- California carries a flat 8.84% corporate income tax rate, with a minimum franchise tax of $800 even for businesses with no taxable income. For S corporations, California applies a 1.5% rate instead.

- Alaska tops out at 9.4%, applying a graduated scale that starts low but climbs steeply for corporations with large taxable income.

New York and Pennsylvania Are Worth Watching

New York applies a corporate franchise tax rate of 6.5% for most corporations, though the New York capital base tax and the New York City corporate tax layer on additional costs for businesses operating in the city. The New York corporate income tax rate in prior years has shifted, so staying current matters. Pennsylvania recently reduced its corporate net income tax rate, which sat at 9.99% for years and is scheduled to step down to 4.99% by 2031 under a phased reduction plan.

If your business operates in any of these states, the combined state and federal corporate tax rate can reach well above 30%, depending on your structure and income level.

How Business Structure Changes Your Corporate Tax Picture

Corporate income tax applies at the entity level for C corporations. If your business is structured as an S corporation, a limited liability company (LLC), or a partnership, income passes through to your personal tax return instead. That changes which rates actually matter for your situation.

For pass-through entity owners, the state corporate income tax rate is largely irrelevant. What affects your bill is the state's personal income tax rate, applied to whatever share of business income flows to you as an owner. A state with no corporate income tax but a high personal income tax rate may offer less relief than it appears on the surface.

Worth noting: some states still create state-level obligations for pass-through entities even without a formal corporate income tax. California, for example, charges S corporations a 1.5% franchise tax on net income, and the $800 minimum franchise tax applies regardless of profitability or entity type. So "no corporate income tax" does not always mean zero state tax for an S corp or LLC operating there.

The right structure depends on your revenue, ownership, and goals. A qualified tax professional can model which combination of entity type and state minimizes your actual burden, beyond the headline rate.

This content is for general informational purposes only and does not constitute legal or tax advice. Consult a qualified tax professional for guidance specific to your situation.

Tax Nexus: How Operating in Multiple States Affects Your Obligations

When a team member works from home in a state where your company has no registered presence, that employee's location can trigger tax nexus there. This is one of the more common surprises for growing companies with distributed teams.

Here is how the two main types of nexus work in practice:

- Physical nexus is created by an actual presence in a state: employees, offices, inventory, or property. Most states have recognized this standard for decades.

- Economic nexus is newer and broader. Following the Supreme Court's 2018 South Dakota v. Wayfair decision, many states can tax businesses that exceed certain revenue or transaction thresholds within their borders, even without any physical footprint there.

One detail worth knowing: gross receipts taxes run on their own separate nexus rules. Your business could have no corporate income tax nexus in a given state and still face gross receipts tax exposure there, depending on how that state defines taxable activity.

Registering in a low-tax or no-tax state does not shield you from obligations in states where you actually do business. Your real footprint, including where your team members live and work, is what determines where you owe tax.

What Else to Consider When Choosing a State for Tax Purposes

Corporate income tax is only one piece of the puzzle. When you're weighing where to register or relocate your business, a few other factors deserve a close look.

Franchise Taxes and Gross Receipts Taxes

Some states skip corporate income tax but collect revenue through franchise taxes or gross receipts taxes instead. Texas, for example, has no corporate income tax but levies a franchise tax based on a business's margin. Delaware charges no sales tax but does impose a franchise tax on corporations. These levies can add up quickly, so factor them into your total tax picture before committing to a state.

Sales Tax Rates and Local Add-Ons

Sales tax rates vary widely by state and can carry additional county or city-level surcharges. Florida's statewide sales tax rate is 6%, but county surtaxes push the effective rate higher in many areas. Texas has a state sales tax rate of 6.25%, with local additions bringing the combined rate up to 8.25% in some jurisdictions. If your business sells goods or taxable services, this matters.

Workforce, Infrastructure, and Incentives

Low taxes mean little if qualified workers are scarce or operating costs are prohibitive. States often offer targeted incentives like credits for job creation, research and development, or capital investment that can offset a higher statutory rate elsewhere. Weigh the full cost of doing business: the headline tax rate is only one part of that picture.

This content is general information, not legal or tax advice. Rules vary by situation and change over time, so consult a qualified tax professional or employment lawyer for your specific circumstances.

2026 Corporate Tax Changes Businesses Should Track

The federal corporate tax rate has held at 21% since the Tax Cuts and Jobs Act of 2017, but 2026 brings real uncertainty for business owners. Several provisions from that law are set to expire, and Congress is actively debating whether to extend, modify, or replace them.

Here are the key changes worth watching:

- The 20% pass-through deduction under Section 199A is scheduled to expire at the end of 2025, which could raise the effective tax burden for S corps, LLCs, and partnerships if Congress does not act.

- Bonus depreciation has been phasing down since 2023 and dropped to 40% in 2025, affecting how quickly businesses can write off equipment and capital investments.

- Proposed changes to the global intangible low-taxed income (GILTI) rules could affect U.S. companies with international operations, potentially raising their federal tax obligations.

- Some legislators have proposed raising the federal corporate rate back toward 25% or 28%, though no rate change has passed as of early 2026.

State-level changes are also in motion. Several states have announced rate reductions tied to revenue triggers, while others are revising their franchise tax and apportionment formulas. Your combined federal and state effective rate can look very different depending on where your business is registered and where it earns revenue.

Given how much is unsettled, it is worth reviewing your entity structure and state registration before year-end, ideally with a qualified tax advisor who can model the scenarios specific to your situation. This is general information, not legal or tax advice. Rules vary by situation and change over time.

Managing Multi-State Payroll and Tax Compliance for Distributed Teams

Running payroll across multiple states means your business faces a different set of tax rules, filing deadlines, and compliance requirements in each jurisdiction. This gets complex fast, especially when employees work remotely from states your company never intended to operate in.

Here are the core challenges distributed teams typically run into:

- Each state where you have employees generally creates nexus, which can trigger corporate income tax, franchise tax, and withholding obligations even if your company is registered elsewhere.

- State income tax withholding rules differ widely. Some states require withholding from day one of an employee working there; others have reciprocity agreements that let employees pay taxes only in their home state.

- Unemployment insurance (UI) taxes are set at the state level, so your rates and wage bases vary by state depending on your claims history and the state's own schedule.

- States with no corporate income tax, like Texas and Florida, still have other levies to track. Texas imposes a franchise tax on gross receipts, and Florida has its own sales tax and county-level surtaxes to account for.

The most common mistake growing teams make is treating multi-state payroll as a single-state problem with a few extra boxes to check. Each new state where an employee lives or works is its own compliance obligation, with its own registration requirements, deposit schedules, and filing forms.

Staying organized means registering in each state where you have nexus, keeping your withholding calculations current as state rates change, and aligning your records at year-end across every jurisdiction your team touches. Consulting a qualified tax professional before expanding into new states can save considerable time and cost down the road. This is general information, not legal or tax advice. Rules vary by jurisdiction and change over time, so consult a qualified tax adviser for your specific circumstances.

Final Thoughts on Corporate Tax Rates and What They Mean for Your Business

State corporate tax rates tell you part of the story, but gross receipts taxes, apportionment rules, and your business structure fill in the rest. A state advertising zero corporate income tax may still create real tax obligations depending on how you earn revenue and where your team is based. The smartest move is to look at your total burden across every jurisdiction where you have a footprint, including states beyond your registration. A conversation with a tax professional can help you model the actual numbers for your situation.

FAQ

What's the difference between states with no corporate income tax vs. states with the lowest corporate tax rates?

States with no corporate income tax (Nevada, Ohio, South Dakota, Texas, Washington, and Wyoming) still collect business revenue through alternative structures like gross receipts taxes or franchise taxes, so your actual burden depends on revenue volume and industry. States with the lowest corporate tax rates, like North Carolina at 2.5%, tax net income directly but at a rate low enough to rival zero-income-tax states for many businesses. The right comparison is total effective tax cost across all levies, not the headline corporate rate in isolation.

Should I register my business in Texas or Florida for tax purposes?

Both states have no corporate income tax, but they differ in how they collect from businesses. Texas applies a franchise tax on gross revenues above $2.47 million at 0.75% for most businesses, regardless of profitability, while Florida charges a flat 5.5% corporate income tax rate on net income with no gross receipts equivalent at the state level. If your business has high revenue and thin margins, Florida's net income approach may work out cheaper than Texas's margin tax structure.

How do I know if my business owes taxes in a state where we're not registered?

Your tax obligations follow your actual footprint, not your incorporation state. If you have employees working remotely in a state, inventory stored there, or sales exceeding that state's economic nexus thresholds, you likely owe taxes there. The Supreme Court's 2018 South Dakota v. Wayfair decision expanded states' ability to tax businesses with no physical presence, so even a fully remote team can create multi-state tax exposure worth tracking.

Does the federal corporate tax rate change based on which state I operate in?

No. The federal corporate income tax rate is a flat 21% on taxable net income for C corporations, and it applies regardless of your state. State corporate taxes are separate obligations layered on top. A business in a state with no corporate income tax still owes the full 21% federal rate; it simply avoids the state-level charge.

Can multi-state payroll compliance be handled without registering separately in each state?

No. Each state where you have employees generally requires its own registration for withholding taxes and unemployment insurance, regardless of where your company is registered. States with no corporate income tax, like Texas and Florida, still require payroll tax registration and compliance for employers with workers there. Bolto's payroll infrastructure automates state-specific withholding, filings, and new-hire reporting across all 50 states, reducing the manual burden of tracking obligations in every jurisdiction your team touches.